Car Loans: Should We Be Worried?

First, a caveat and a reminder:

Caveat: I am not an auto finance expert, not by a long shot. I buy all my cars with a pile of Ohio Lottery scratch-off cards.

Reminder: I have an optimistic bias regarding the American new-car market, seeing it as more resilient than most other observers.1

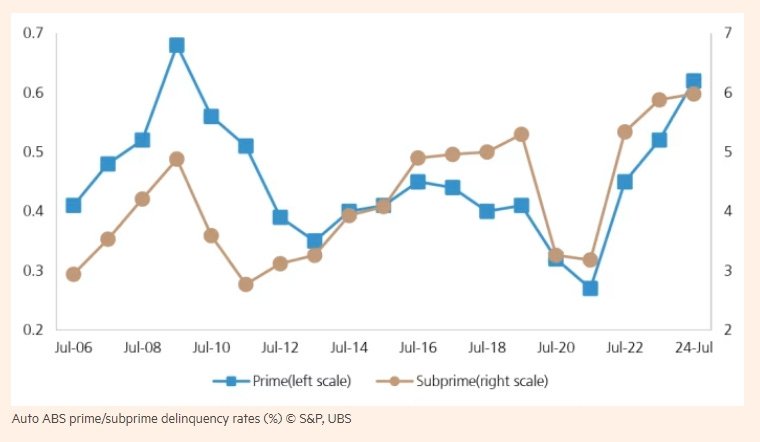

With those admonitions out of the way, I note that there has been an uptick in anxiety about car loans in the USA: as delinquency rates edge up, are we on the verge of a Carpocalypse, where loan defaults cascade and contribute to a slide into recession?2 Given my lack of expertise and my upside bias, I liked the recent analysis given in the Financial Times, “Is the surge in US auto loan defaults to 15-year highs a reason to panic?”. Bryce Elder recently reported there that, courtesy of S&P and UBS, auto loan3 delinquency rates in the States are up sharply. See the first chart below.

(Note, please, that the left and the right axes, both showing percentages of loans delinquent, are on different scales!)

Prime loans (prime + super prime) make up about 85% of all new-car loans, near-prime 10%, and subprime and worse, 5%, according to Experian.4 And we can see here that subprime delinquencies are up to 6%, and prime up to 0.6% (sic). Recall that delinquency is triggered when a loan payment is just one day late.

AUTO LOAN DELINQUENCIES

Looks pretty scary, reminiscent of the levels we saw during The Great Recession.

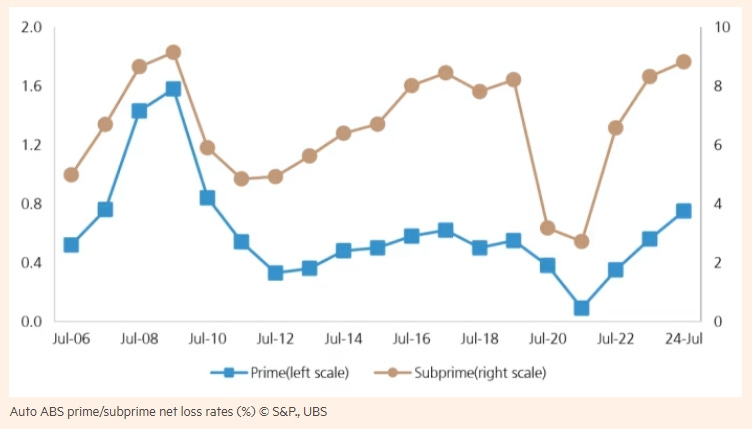

But maybe not. The FT adds another chart, showing actual default rates, expressed here as net losses. The definition of “default” varies by situation, but boils down to being triggered when the borrower misses several payments in a row, greatly increasing that the loan will not be repaid in full. Note that default/net loss rates for prime buyers, which as I said represent the great bulk of new-car buyers who take out loans, are not up as sharply as delinquencies, thus not retracing the path followed during TGR. (Subprime is looking bad, indeed, but again, these loans are only about 5% of new sales that are financed.)

AUTO LOAN DEFAULTS / NET LOSSES

The FT reports that UBS believes that prime borrowers are choosing to resume payments once they miss one, this time around at least, to avoid losing their cars. As the old saying goes (flagged in the comments section of the FT article), “You can sleep in your car, but you can’t drive your house to work.”

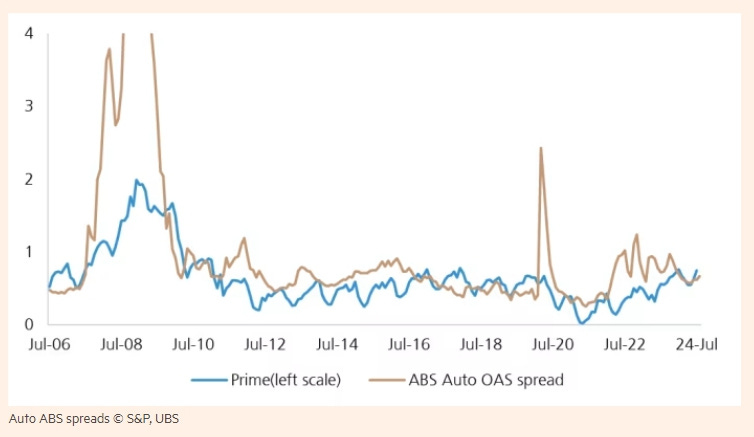

But given my lack of expertise, let me defer to The Ultimate Authority here, The Market, showing you one last chart, of ABS (asset-based securities) spreads:

ABS AUTO SPREADS

As Elder writes, “Spreads on auto asset-backed securities (which track losses, not delinquencies) have widened a tad recently but remain approximately half the long-run average of 1.12 per cent.” Simplistically, wider spreads imply a greater risk of default. So The Market remains pretty unflustered, though of course a) The Market could be wrong and b) The Market could change its mind.

Net net, two tentative conclusions I draw5:

In the short term, new-car auto loan statistics are not looking too worrisome, especially when we look at prime loans, the vast bulk of new car loans.

In the long term, this is all support for my hypothesis that the new-car market is continuing its “premiumization” (see earlier posts here and here), as a larger and larger share of the new market is purchased by wealthier and wealthier people. This doesn’t mean that the new-car market has become immune to economic cycles (good Lord, no!), but maybe it is a little… vaccinated?6

That’s it for today: I have to run over to Michael’s Diner and grab some more scratch cards, as my lease payment is due.

This should be a signal to all of you to short OEM stocks at once. Kidding! Not investment advice!

Check out the online prediction markets for bets on whether a recession is likely, e.g. Metaculus . Keep in mind, however, the first rule of predicting recessions: all statements about recession predictions are wrong… including this one.

Typically, these rates include loans and leases combined.

For USED cars, near-prime-and-better loans make up about 75% of the total, with subprime at about 25%. Also, we are talking here about percentages of financed cars (loans and leases): a significant portion of new sales are actually paid in full in cash (20-40% of purchases, in different years).

But must I remind you of the caveat again?

Don’t even start with the comments on this joke, ok?