EV Perspectives, Part Deux

I hope you enjoyed the first round of these. Here is the second, with a third to come later this week. As always, my gratitude to the analysts who provide the insights I garble for relay to you!

For our fourth view we turn to J D Power, and their excellent price elasticity of demand analyses. Their point, in essence, is that in some respects contrary to accepted wisdom, EVs in the USA have less of a price problem than a product problem. That is, price cuts alone won’t do much for EV demand unless the EV product is attractive. This is shown by their calculations of relatively inelastic demand for EVs1. (An example of a very inelastic demand is for salt: if the local grocery store cuts the price of salt in half, it is likely almost no one will buy any more salt - they just don’t need or want more, at any price.) Thus we saw strikingly weak demand response to Tesla’s strikingly massive price cuts.

This problem will ease as more and more EV models are launched into more attractive segments, such as compact SUVs.

But before we get too excited about the EV product cavalry arriving, note the problem that we may need new cavalry on a regular basis. That is, Americans are used to now, and expect, more and better EV models to regularly proliferate. Meaning that the novelty of a model is crucial to demand: once it’s been on the market for a few months it’s time to look at a rival’s even newer and better (longer range? faster charging?) model launches. The implication is that an OEM cannot just introduce the next generation of (e.g.) the Golf, and then expect it to run strongly for a few years - the OEM may have to launch the next Golf in just a year or two, or less. This rate of product churn is very expensive and adds to the ICE/EV profit gap. Bernstein illustrates the problem with their chart of how quickly the average EV model loses market share:

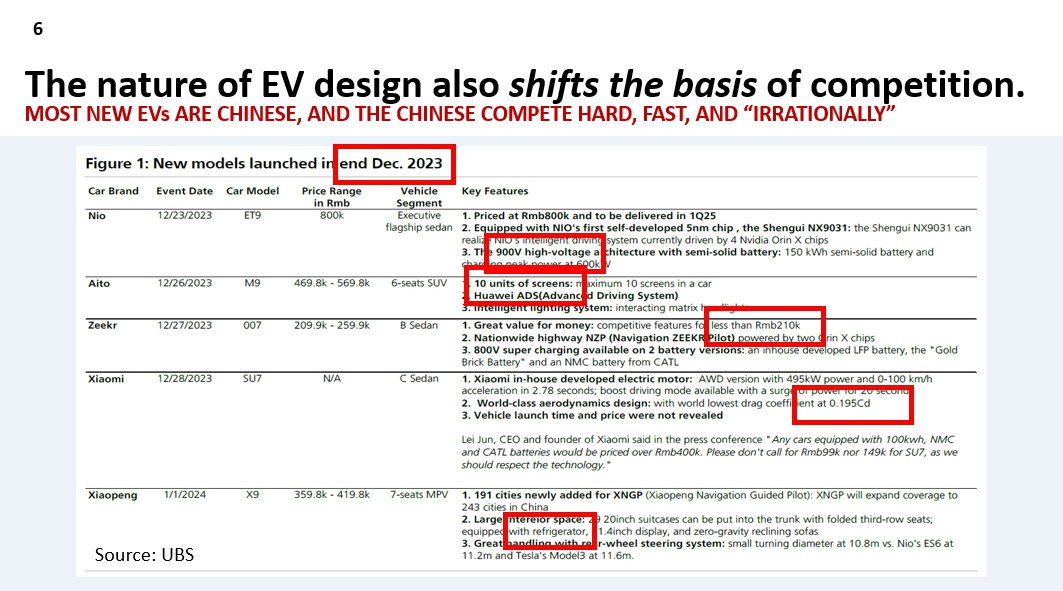

Further intensifying the competitive battle (great, just what we needed) is the Chinese in particular seizing upon the product flexibility inherent in EVs (better packaging, limitless onboard electrical energy, etc.) to try changing the basis of competition. Some of the old competitive metrics (HP, 0-60 times) have been rendered almost irrelevant by the advent of EVs, and now there are new ones which incumbent OEMs are less familiar with. Check out this UBS chart of recent Chinese EV product innovations:

I am not saying incumbent ICE OEMs can’t compete on screen counts, voltages, refrigerators, and more, but that these are novel dimensions of competition, and ones that shift rapidly over time2. Agility will become even more valuable now.

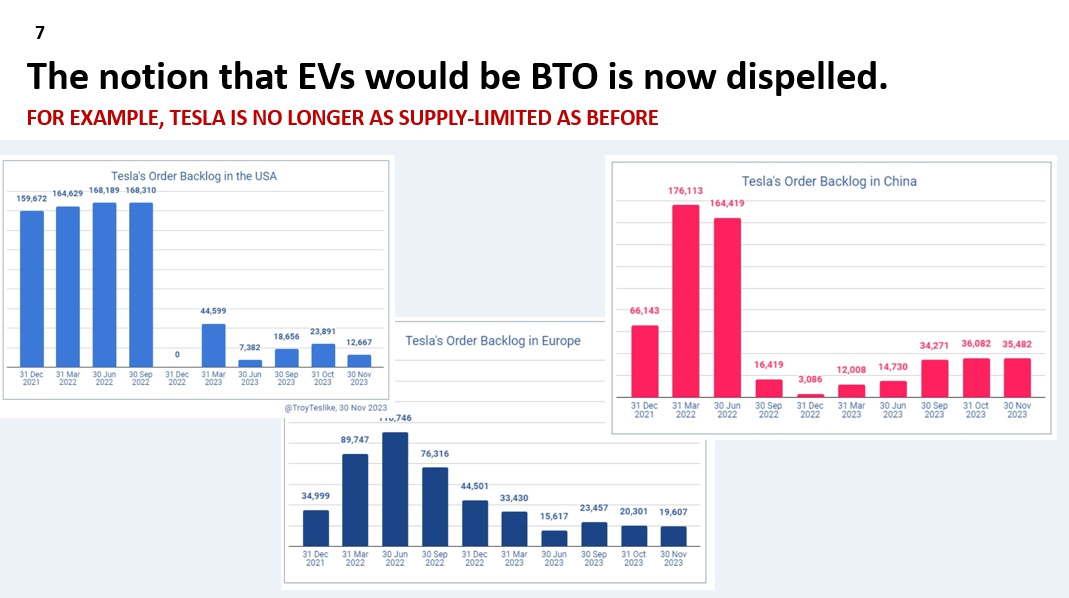

Okay, last for today: remember a few years back (especially in the midst of the pandemic), when some executives believed that EV customers and EV manufacturers were somehow aligned in the belief that the future of EVs would be BTO3 (build to order)? That the plants would be agile enough to not have to build in batches (or to stock), and that customers would be happy to wait for their car to be built (versus buying off the lot, or from the production pipeline)? Well, I guess not. Even Tesla seems to be, let us say, edging away from BTO. (Bernstein has estimated that indeed 25-40% of Tesla demand worldwide is now met from in-transit or on-the-ground inventory.)

I do believe that we have moved to a more BTO environment, I do believe that factories are more flexible now, and I do believe that more customers are happy to order. But there seems to be no wholesale stampede towards waiting. Instant gratification is still very attractive… just look at binge-watching the latest Netflix series!

See you later this week. If you can wait. (BTO joke.)

Thus my use of the Greek letter eta, η , which is often used to denote elasticity.

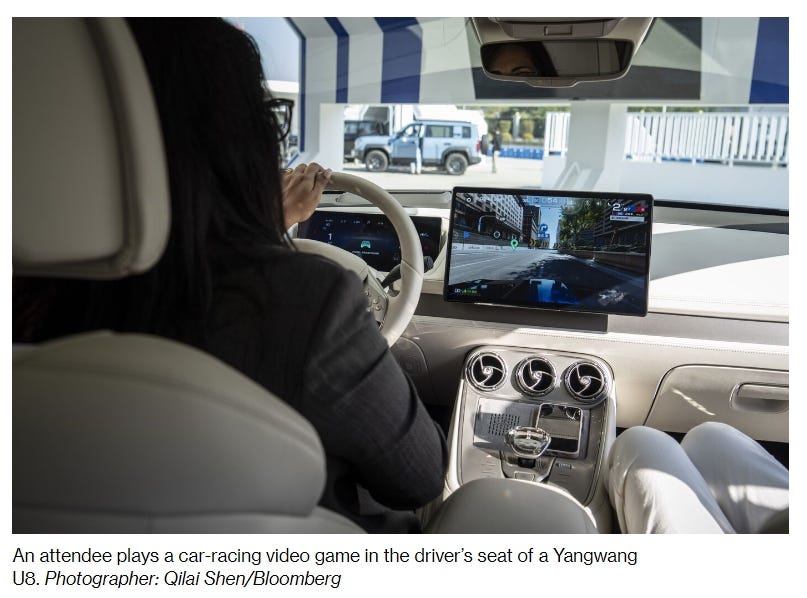

Note BYD’s recent launch of a vehicle which lets you power up Grand Theft Auto (or a similar game) on the screen (while the car is parked!), then disconnect the car’s pedals and wheel from CAR operation and connect them to GAME operation. Voila, your parked car is now a GTA simulator! (Yangwang is a BYD brand.)