Holiday Chart #8

An ongoing discussion topic in the world of American auto retailing is “consolidation.” A general consensus has emerged, based on a quasi-religious belief in economies of scale, that the new-car dealership industry must steadily consolidate into fewer and fewer players, as the large out-compete the small. There is some debate as to how fast this will occur, but I have never met anyone who thinks the process will stop, or God forbid, reverse.

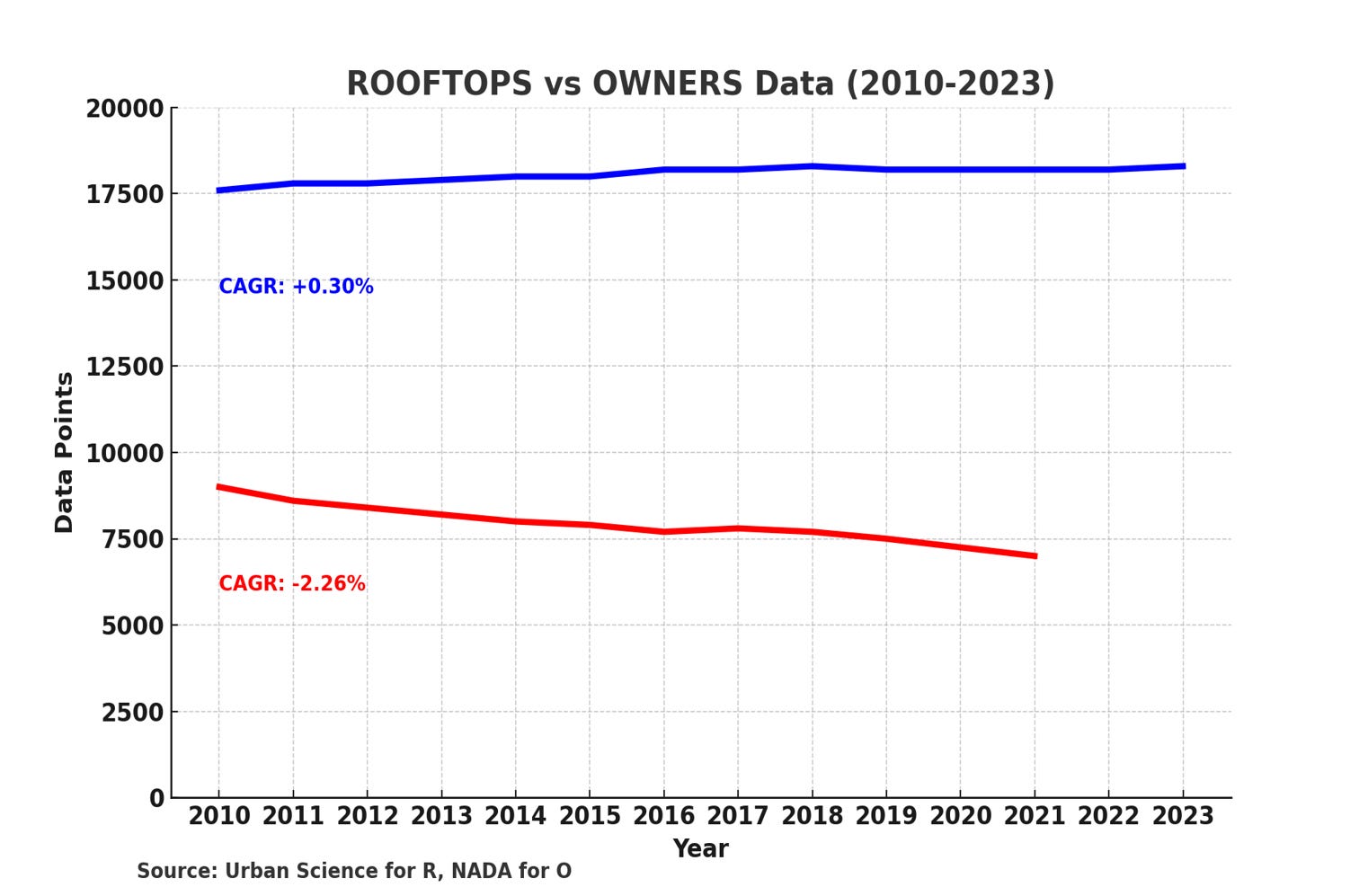

A problem with this discussion is that most people involved tend to mix up their terms. There is consolidation of the number of dealerships aka rooftops aka stores, and consolidation of the number of owners of those businesses. The two processes are proceeding at very different rates. Chart, please!

As should be obvious, rooftops are not consolidating at all. We thought they might, because the internet would allow every buyer to shop every store, and so eventually (in theory) we might end up with one giant Chevy store that drove everyone else out of business. Didn’t happen: geography matters. Customers want local access and suburban sprawl kept going, so store count has remained dead flat for over a decade now.1

Owners, however, are consolidating. Maybe not to the extent predicted in the 1990s (when it was thought that public chains in particular would sweep the board), but it has been a pretty steady exodus, at perhaps 3% annually now. (Issues of data confidentiality prevent us from displaying figures for 2022 and 2023, but we have no reason to believe the trajectory has altered.) There are many reasons for this type of consolidation: some owners not wanting to bet the family fortune again (e.g., on EVs), others facing complex succession issues, and of course there is the presence of active buyers. (Remember, for every dealer selling to get out of the business, there is some buyer eager to get in.) But to date it is still a pretty slow process: we’ve moved from about 2 stores per owner to about 3, in a decade or so. The pace may pick up, I don’t know: talk to experts like Haig and Kerrigan for more insights on this.

The point is, depending on what definition you are using, this industry is either not consolidating at all, or consolidating - but slowly. Taking both trends together, it looks like the “small” 2- 3- or-4-point owner may have many good years ahead of her or him still.

Dad Joke of the day:

Patient: “Doctor, tell me the truth, I can take it!”

Doctor: “You’re in a bad way, you have only 10 to live.”

Patient: “Huh? 10? 10what? Months? Years?”

Doctor: “…9...8….7…”

This was not always the case! We are way down from peak rooftops, as this bonus chart shows. The decline from the 1950s peak was driven by numerous factors (exits of smaller OEMs, yes economies of scale acting on the smallest stores, rural population collapse, bankruptcy of arguably over-dealered GM and Chrysler, etc.). But these factors seem to have played out. For one thing, with the average rooftop generating over $70,000,000 in revenue now, the “Mom and Pop” store is mostly gone. And where they remain, inefficient as they may be, they are protected by geography: the small Chevy store (e.g.) in a remote rural area faces limited competitive pressure.