An EV Update

Now that some dust has settled...

Ground rules: In this post I am leaving aside the noisy extremes of the US EV debate (“Electric vehicles are humanity’s destiny” versus “Electric vehicles are a tool of government oppression”), and focusing just on the actuality of where the American EV market stands right now. I decided to post this update in March 2026 in order to allow the demand picture to normalize somewhat, after EV market share first jumped up in anticipation of the the Federal tax credit ending last Fall, and also after it moved down in the hangover from the sales that had been pulled ahead. Where are we now?

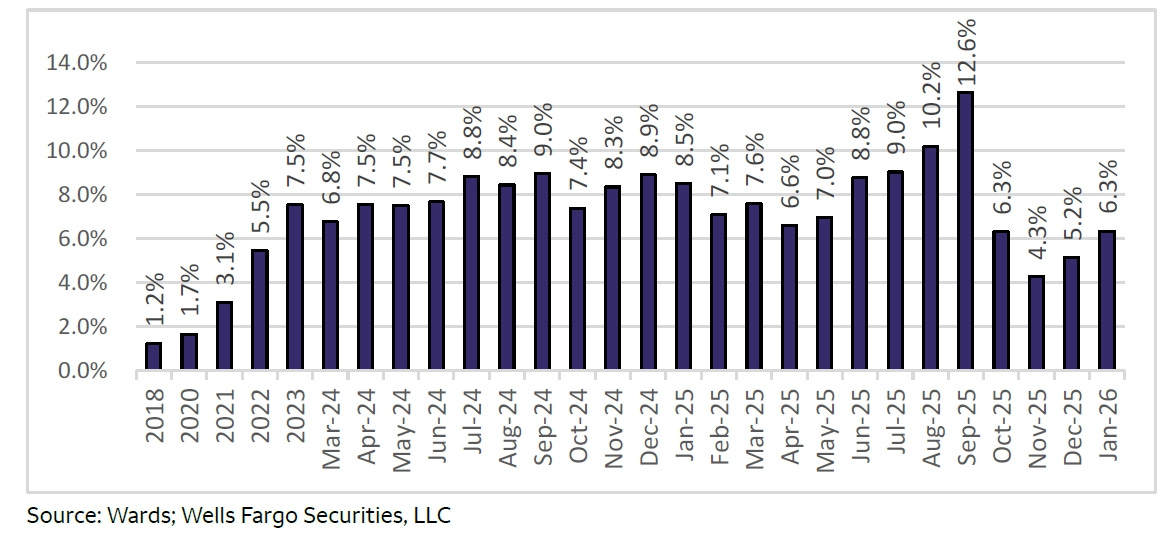

To answer that question I use, courtesy of Colin Langan at Wells Fargo, this chart based on data from Ward’s:

BEV MARKET SHARE OF USA AUTO SALES

The “beat the expiry” binge took us to almost 13%, and then the hangover dropped us to almost 4%. Brutal.

By the way, I use this particular data source because it is consistent over time, so the numbers are comparable. Please note that depending on your favored data source, YMMV (your mileage may vary), since other sources will add in PHEV to BEV numbers (and get thus EV), and in extreme cases will count HEV as “electrified” as well. And other sources may use registrations versus sales, etc. Then we have commercial fleet versus private vehicles. Anyway, I think all the varying sources will show the same underlying pattern, broadly speaking.

And that pattern is:

EVs were very niche low-end short-range urban warriors (mostly Nissan Leaf, and who can forget the original Honda Insight) through the 2010s, until Tesla let the genie out of the bottle with the Model S (the first “upscale” EV, where you did not have to sacrifice style, speed, or range while you were saving the planet from the comfort of the California HOV lane). Turns out you can disrupt “from above,” not just “from below” (which is how I understand the original Clayton Christensen definition of the D-word).

EV sales leapt up and then were kept up in the air by various financial incentives (e.g. the Federal tax credit to buyers, emissions credits to A Certain OEM, etc.), assisted of course by steady improvement and enlargement of the range of vehicles on the market1. The current administration gutted all these various financial incentives, and the market has settled down to where it was in 2022-2023.

So, where do we go from here? After years of overly-optimistic forecasts for EV penetration by almost every pundit (with the notable exception of the Anderson Economic Group), prognosticators are now more cautious. My gut feel (or should I update my jargon and call it my vibecast?) is that we’ll add a percent or two of share annually for the next few years. The products are better than they were, the EV/ICE cost gap seems essentially gone, it’s no longer a high-beta one-company (or should I say one Technoking?) game, the charging networks are expanding, the political furor around EVs seems to be abating, and as the installed base expands, more consumers are growing familiar with this previously-alien technology2.

As the saying goes, we will eventually “solve for the equilibrium.” Which might in the near term be something like diesel-powered duallies on the ranches, gas-burning pickups in the ruburbs (rural suburbs), BEV runabouts in most urban areas, and PHEVs and HEVs in the closer-in suburbs. Not to mention a diverse zoo of person- and cargo-carrying e-bikes and scooters everywhere.

Oh, and the billionaires will just fly over the resulting traffic jams in eVTOLs…..

Though the mix for too long was tilted toward the expensive, premium end of the market, since every other OEM wanted to be Just Like Tesla. We have been paying the price for this stampede ever since, so that only recently have OEMs been launching waves of cheaper (euphemistically called “affordable”) electric products.

Believe it or not, about 20 years ago I was talking to a person who actually thought that electric cars ran on very very long cords. This person was not known for his Thinking Things Through, but the image has stayed with me….