Auto Insurance: Competitive Interference

Your brain isn't a filing cabinet, it's a popularity contest.

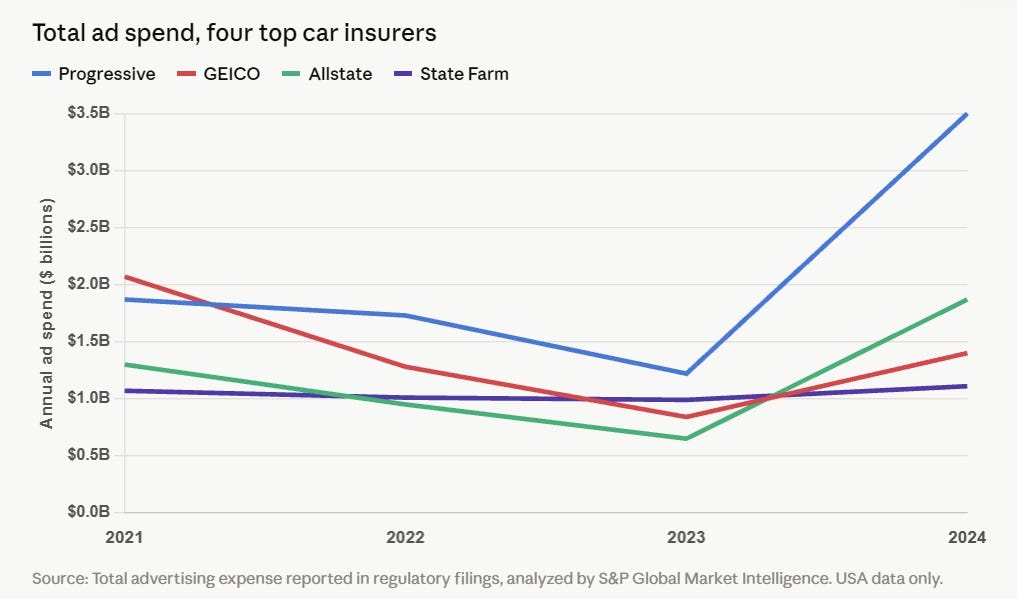

Sarcasm alert: you may have noticed online or on TV or at the baseball stadium one or two advertisements for car insurance. Here and there. For some reason, these ads are populated mostly with mascots. A Gecko, an Emu, a Flo, etc. The top four car insurers in the USA (GEICO, Progressive, Allstate, and State Farm) have about a 60% market share among them1, so it’s not like any of them are advertising because they are obscure startups looking to be noticed. And they compete in a highly regulated industry, so it is hard for an ad to differentiate their product. And yet they spend about $8 billion a year2 mostly just telling you their own names, often via spokesanimals3. That works out to about $30 a year for every existing car insurance policy in America.4

So why the heck do they do this? You already know their names, you know what they do, you can easily find them, and their market concentration is so high there’s a 60% chance that you’ll end up with one of them regardless of any advertising. Baffling, at least to me.

I have always wondered about this, and much to my relief have stumbled on an excellent paper by Sahni and Yang, Consumer Memory and Competitive Interference: The Case of Auto Insurance Advertising, which explains it all. Much to the detriment of those who believe American consumers are careful shoppers who devote significant time to evaluating their options!

I won’t go into the methodology of their work5, and as always encourage you to read their paper, as I will inevitably in this brief post distort or garble their findings. Which I interpret as:

1. Your brain isn’t a filing cabinet, it’s a popularity contest. We don’t store “GEICO” and “Progressive” as separate facts we can look up on demand. They’re linked to a mental folder called “auto insurance,” and when that folder gets opened, the brands inside it compete to be the one that surfaces first: word-association, not database lookup.

2. Recall is a habit, not a fact. Every time a brand successfully surfaces in your head, that pathway gets a little stronger — like a hiking trail that’s easier to walk the more people use it. Every time it doesn’t surface, the pathway fades a bit, gets overgrown. Forgetting isn’t really about time passing, it’s about other stuff crowding in and winning the competition for our attention: the “competitive interference” in the title.

3. This means advertising a brand actively suppresses recall of its competitors: an ad’s job isn’t (only) to build up GEICO’s stock of goodwill — it’s to push Progressive further back in the mental line.

4. This explains the relentless repetition: the moment GEICO goes quiet, its trail starts fading and a competitor’s trail gets relatively easier to find. This is a different economic logic than “advertising = information delivery;” it’s more like “advertising = mowing the lawn, over and over.”

The paper backs this up with results of what looks to me like a very robust randomized experiment against online advertising exposures.

(For the wonks among you, check out this one specific experimental finding that supports the authors’ core hypothesis: when other competitors advertised more, in response to a first competitor’s ad campaign, the first competitor’s ad’s effect got stronger, not weaker. That is, say, after the start of the baseball season, when insurers flood broadcast and in-stadium media with ads, GEICO’s earlier ad became more valuable to GEICO once Progressive launched its own campaign a week or two later. The way I would have thought about this was that more competitor ads should drown out my own ad. But in the author’s model and work, competitor ads mostly serve to reopen the “auto insurance” mental folder!)

Time for disclaimers and caveats. To argue against these findings, note that the core evidence comes from a single one-day banner-ad experiment, it was run in 2015 on one website, and compared just two insurers. To argue for the authors, their work rests on a well-established, decades-old body of cognitive psychology on memory interference, their underlying methodology looks very sound, and their paper’s out-of-sample tests (don’t ask!) independently confirm the same pattern using a completely different data source.

If you’re with me so far, I’ll wrap up with this:

This paper provides the best explanation I have ever seen as to why we are inundated with emus and geckos. And it is this: these ads aren’t fighting to change our minds; they are fighting to be the name that pops into our heads (at the moment we are thinking about shopping for insurance). And every dollar the gecko spends doing that is a dollar that makes it a little harder for us to summon up Flo instead.

Thus, we are doomed to see over and over again all these same ads, forever. And it is perfectly rational for these insurers to be doing this. Much to my dismay.

Note 1: yes, my good AI friend Claude helped me out with this.

Note 2: advertising professionals who read this blog, if any, please weigh in with corrections and comments!

Data from NAIC, National Association of Insurance Commissioners.

Data from S&P Global.

I am claiming authorial rights to this word.

LexisNexis and NAIC data, author’s calculations on same.

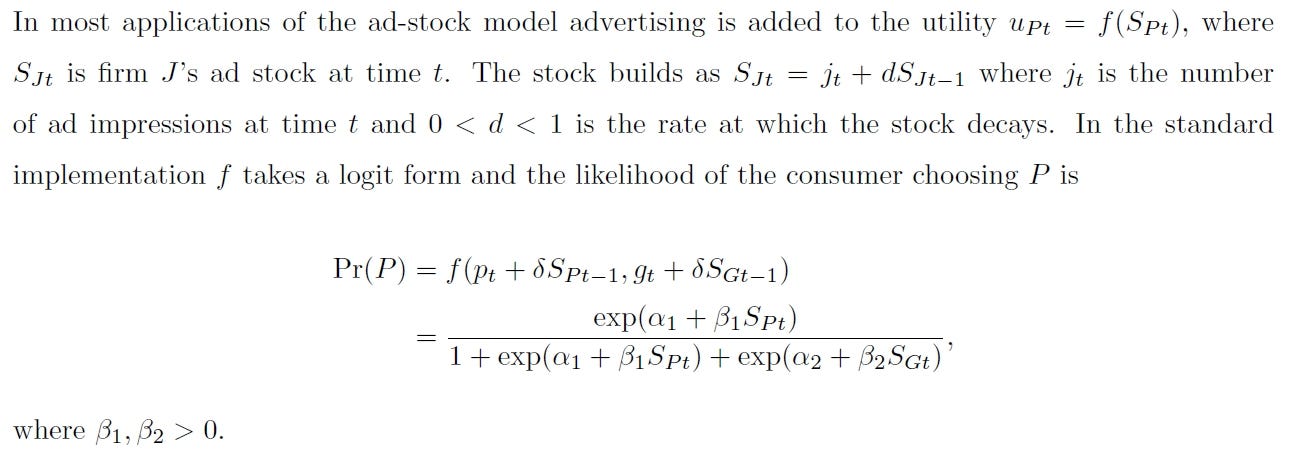

Partly so as not to bore you, but mostly because equations like this fry my brain:

Well, of course, only when both of those are greater than zero! I guess…. 😀