Holiday Chart #6

Welcome to the jungle...

Yet Another Disclaimer (YAD): Betting against Tesla has been, to put it mildly, a losing proposition over the last decade. Even talking about Tesla is close to pointless, as the conversation is essentially an excuse for everyone to repeat deeply-held opinions they are never going to change. So this post won’t even try to forecast the company’s fate or share price.

But as I’ve been involved in the let-us-call-it more “traditional” automotive business for a few decades, I will take it upon myself to welcome Tesla to our club. The time has come for Tesla, which turned 20 this year, to be given the hidden password and secret handshake necessary to enter. It’s the club of incumbent old-school dinosaur OEMs, with members in America, Europe, and Asia. And the club’s distinguishing feature is that its members, with the exception of some fancy types like Ferrari, just don’t make very much money.

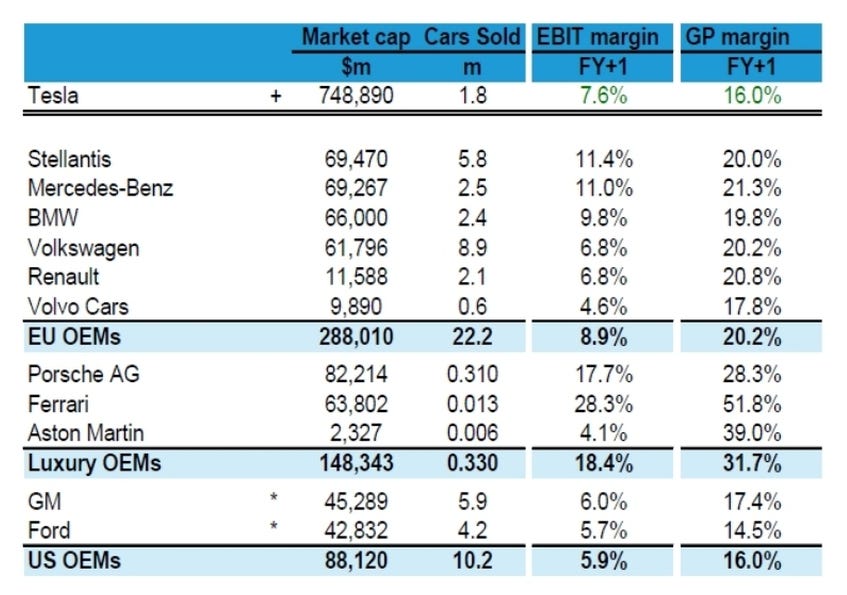

Here’s the list of club members:

(Note: as per Bernstein (Mr. Sacconaghi specifically), the Tesla numbers are 2024E including EV credits, compared to forward year numbers for comparable OEMs. Sources include Bloomberg data as of December 4, plus company filings and Bernstein analysis. My thanks to all involved.)

Pick your margin, either EBIT or GP, and you see that the new member has profitability really undistinguishable from that of the old crew1. Maybe Tesla’s numbers will bounce back (like a steel ball off a Cybertruck window) - see YAD, above - but lately it seems like mass-market gravity has brought them down to the club’s standard. Welcome!

Twas’ not always thus: as Mr. Sacconaghi points out, Tesla automotive gross margins were over 20% in Q1 2020, 22% in Q1 2021, and 30% (!) in Q1 2022. But the company’s automotive gross margin has actually fallen every quarter now since Q3 2022. There are many overlapping explanations for this decline, but most of them (IMHO) can be lumped under the heading of “entry into the mass market entails dealing with the competitive dynamics of the mass market.” Tesla’s lower prices and higher volumes of recent years jointly have transformed the company into a mass-market player. Congratulations! But those mass-market dynamics include consumer expectations of rapid model refreshes, extensive model proliferation, choosing cars from massive inventories, head-to-head price competition, and more - all of which conspire to suppress returns.

So, welcome to the jungle2, Tesla, the place where incumbent OEMs beat each other around the head with discounts and incentives and advertising and fleet sales and push production and leasing deals and all that rough-and-tumble stuff that makes it so hard for them to ever cover their cost of capital. And while you’re getting settled, please sign up for one or more of the club’s activities, which include Axe the Flopped Model, Regulatory Roulette, and the ever-popular Bankruptcy Night3. Never a dull moment at the OEM club!

Dad Joke of the day: “Two guys walked into a bar. The third one ducked.”

Of course, Tesla’s market cap is off the charts, but that’s a more… complex… topic.

Pretty clever, eh, quoting in an automotive blog a song by a guy named Axl!

Don’t worry about that, club members usually get bailed out. Government Rescue Request forms are available at the front desk.