Yet more affordability chatter

This will be quick. As mentioned before, I am a mild skeptic re the affordability “crisis.” I do realize for many millions of Americans inflation and job insecurity and excessive debt carrying costs are very real issues and operate to absolutely exclude them from most if not all of the new-car market. But as I believe that the new-car is mostly shopped by wealthier Americans, I don’t see the relative dearth of low-priced new cars as as big an issue as others do1. And wealthier Americans are doing pretty well, and thus the new-car market is also doing pretty well, as far as I can see. (That is, without access to the vast data sets that firms like Cox and JDP have. I can only lob in my opinions from the sidelines, as it were.) In terms of both pricing and volumes, we are above where most forecasts from last year would have had us by now.

And I just came across, thanks to the wonderful weekly blog of Charlie Bilello, more evidence for my belief that the well-off will remain strong buyers of new cars. (If you don’t subscribe to his blog, you are really missing out! Loaded with info about financial markets.)

Accepted Wisdom is that one reason we have an affordability crisis, if we do, is that high interest rates are suppressing demand for new cars, by raising monthly payments. And of course this is true, but the question is to what extent is this a problem? My belief is “not as much as one would think,” because the average new car buyer is wealthier than the average American, and can more easily weather higher rates. (And I believe wealth is as or more important for car buyers as income, as mentioned in an earlier post.)

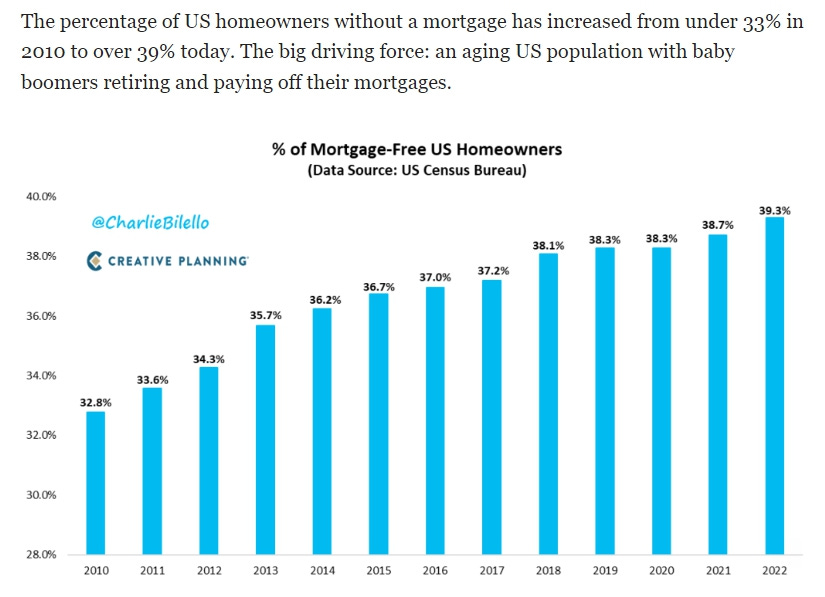

And - now we turn to Bilello charts - it isn’t just wealth at play, but how insulated that wealth is from interest rates. It turns out for many better-off Americans (e.g., those who own homes), the level of insulation is high, partly because they have built up real-estate equity:

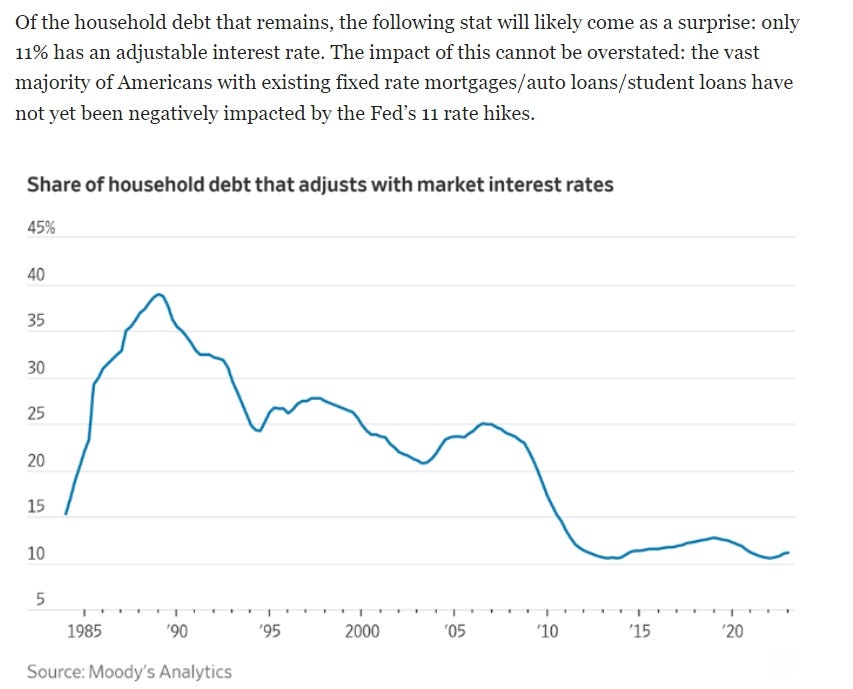

(Recall, tangentially, that the average American new-car buyer is about 54 years old, so she or he has had time to draw down the mortgage.) And to further build on the point, what debt remains is itself insulated from rates, to a great extent:

I left Charlie’s commentary intact because the implication for the new-car market is crucial, if my chain of reasoning is correct. And that chain goes like this:

The average new-car buyer is older than the average American (54 versus 38 years old)…

The average new-car buyer is wealthier than the average American (especially by virtue of having built up home equity over time)…

The debt that the average new-car buyer is still carrying is relatively insulated from recent interest-rate hikes (as much of it is at fixed rates set quite a while back, especially in the case of mortgages)…

And therefore the average new-car buyer is not as likely to be driven from the market by the current high level of rates.

Of course, it costs any buyer more per month to buy a new car when rates are high. Of course! But in the broader scheme of things, that (wealthy) buyer is not feeling the pain of higher rates to the extent the financial headlines will assert. To put it simply, if I have paid down much of my mortgage (and so am sitting on significant real estate equity), and if what debt I do have has not gone up in price, I am more willing to splash out on a new car than otherwise - even if the new car’s loan is costlier.

I promise to shut up about affordability now. For at least a week. Maybe.

Given my forecasting track record, this probably means the SAAR will collapse to 2 million within hours of this post….