My thesis today is that the new car market (in the USA at least) has become a premium market. It is still of course a mass market in that millions of cars are sold, but hey, Hermès (to pick just one example) generates about a billion dollars in revenue in the USA annually, which makes them simultaneously “mass” and “premium” also. And there are implications for the entire industry of this mass upscaling, as I will point out at the end of this post.

What evidence do I have for this assertion? Mostly circumstantial, as a court of law would say, because we don’t really have a definition for “premium,” and it shifts over time anyway: a 2022 Camry teleported to 1952 would outperform everything on the market in terms of ride comfort, climate control, audio systems, and any other indicator of luxury (except, okay, no Purdy shotguns in the trunk boot). So let’s lay out my motley list of arguments, and you can decide for yourself:

Back in 2000 we sold about 17 mm vehicles, to a population of about 280 mm; in 20191 we sold 17 mm to a population of about 325 mm, thus going from 6% penetration to 5%, and I cannot believe the smaller segment is not a richer one.

In support of that, we know that the average household income in the USA is about $65,000, but for the average household buying a new car it’s well over $100,000 (various sources, e.g. Strategic Vision, government data)

The mix of vehicles sold is enriching as well: Autodata has the USA premium market at 9% of total sales in 2000, and 13% in 2019. S&P (IHS) uses a different definition of premium, but its corresponding figures are also 9% and 13%. (By the way, DesRosiers reports 6% and 12.5% for those years in Canada. And here I thought they were all Socialists up North!)

In a related point, the most popular vehicle type in the USA is a premium vehicle: the pickup truck. As TrueCar has pointed out, Ford sells many more vehicles in the USA over $50,000 than Mercedes does, and that is because the pickup truck has become the New American Luxury Vehicle.2 Full-size truck prices are closing in on $60,000, while typical sedans (remember them?) and crossovers languish in the $30,000-$45,000 range.3

And OEMs have been slashing their offerings of lower-priced cars (a trend accelerated during the chip shortage, but it was under way before): JD Power tells us in 2015 over 20% of new vehicles on offer had MSRPs under $20,000, but by 2019 that had fallen to 12.5% (and during those four years low inflation had no time to move all MSRPs up).4

Okay, so only the well-off are buying new cars, more or less. And they can certainly afford them: the Census Bureau tells us that the average household income of the upper quintile of Americans was $125,000 in 2020 dollars in 1965 — and now is double that, at $250,000 (fodder to the Inequality Debate, which I will not touch here!)

But since there are still about 285 mm vehicles on the road in the USA (as Experian tells us), we know Americans are still driving something (we’re still at about 2.5 cars/household5), and so there is demand for wheels. And what the average American is buying is increasingly a used car, over 20,000,000 annually, says Cox Automotive. This makes eminent good sense: car quality was so poor years ago that to buy used was to admit you were desperate, frankly: the 1970s for example was a decade of corroding mufflers and overheating radiators and one-year warranties. Today, thanks in no small part to the valiant efforts of CarMax, we all know that a low-mileage three-year-old Accord is a very, very reliable and sensible buy. And even the OEMs, who would rather you buy new every month or so, recognize this, with the spread of their CPO (Certified Pre-Owned) programs.

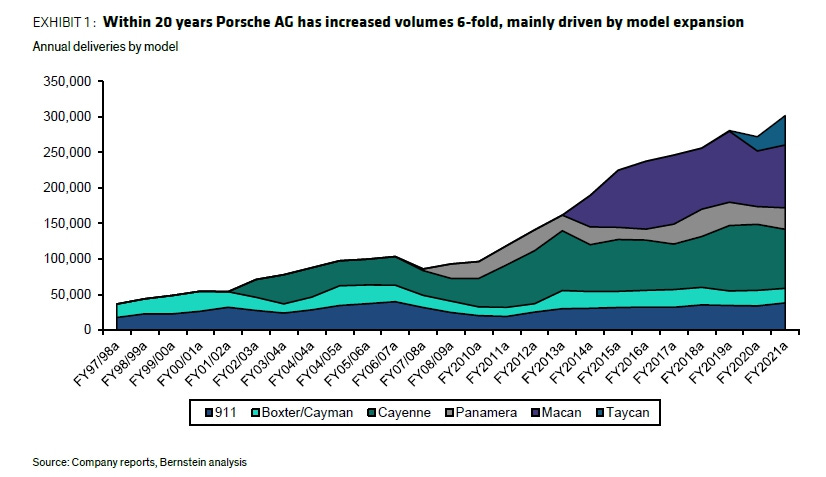

Since there is supposed to be a chart in here somewhere, maybe this one from Alliance Bernstein would be a good one to insert:

Talk about “If you build it, they will come”! (Field of Dreams, 1989) But the demand for a premium badge is so great we’ll line up for Porsche… trucks?6

I will assert that the upscaling phenomenon is almost entirely demand-driven: the wealthy are lining up to pay up for new cars, and the rest of us are quite happy to shift our demand to used cars. Some of you — the more conspiratorially-minded? — might say that there is a supply-side dynamic here, too: that the OEMs are just hiking prices, thus boosting profits, and somehow buyers are meekly following along. Well, if this were true it would be hard to explain the GM and Chrysler bankruptcies, but we have better data than just that. Let’s look at the relative inflation of new-car prices since, say, 1965. If we look at the CPI (consumer price index) for all items, it’s gone up by about a factor of 8 since then. If we look at the CPI for just new cars, that’s gone up only by a factor of 3. Relative to the rest of the things we buy, therefore, new cars have gotten cheaper. So this is not a supply-push development, but one of demand-pull. (And further, we can see the used-car shift in the numbers: the used CPI is up by a factor of 5 since 1965, as demand for used cars grew relatively more.)

Next question: will this continue? Will all new cars be Ferraris by 2040? Well, no, but there are some enormous tailwinds behind this move upscale:

American GDP continues to grow, and more money = more money to spend on cars.

The American population continues to age: and older people are the biggest spenders on expensive cars (as S&P data shows, people over 55 buy over half of all new cars), and the Census projects the number of Americans over 65 will grow from 55 million now to 75 million by 2030.

More speculatively, we see continued growth in single-person households, which may argue for more expensive cars on average (if there is no need to have multiple cars for multiple family members).

It is certainly hard to imagine what will cause the market to shift downwards at any future point, barring some global depression.

So what are the implications of all this, if the trend is indeed real and ongoing? A few things come to mind:

First, OEMs can probably be braver about pricing. All our prior price elasticity models have been destroyed in the last few years (accelerated by the chip shortage: see below). For example, using ALG’s model of a few years back, current price levels should have sent volumes crashing down to 10 million units annually, but instead we are at 15 million and if we didn’t have supply constraints could probably go higher. In the USA at least, it turns out that OEMs collectively have been underpricing their cars for many years. Of course, this happened because each was afraid not to match the price cuts of the others. But when an industry-wide supply constraint emerged, and there was thus no motivation to match price, the true WTP (willingness to pay) of American customers was revealed. Now, how to maintain this? See the Note below.

Second, product lines can (continue to) be moved up, and trim levels with them. Let your CPOs handle the lower end of your market (saving a heck of a lot of product development spend!) and ditch the A-classes.

Third, expect higher profits. Go look up Harrod’s Conjecture of 1936, which says that price elasticity declines with income. Richer people buy more expensive goods that offer higher percentage margins (as well as higher absolute profit dollars). The luxury OEMs have known this for years, and recently Mercedes seems to be making a more vigorous and public commitment to the principle. If you want a newer take on this, see Kunal Sangani’s recent work, showing how much more percentage markup is possible with each upward increment of customer income.

Fourth, if you’re a dealer, you may want to focus more on the premium brands: their future may be brighter than that of the mass-market brands.

Fifth, there may never be a “classical” wave of Chinese exports to the USA. The Japanese came in under the domestics in the 1970s (turbocharged by the oil crises), and then the Koreans in the 1990s. But I don’t think there is any room left in the market for a new wave of cheap imports, because quality used cars have taken over the lower-priced world. So we will see Chinese cars come to America (barring geopolitical incidents…), but not competing on low price this time — rather, more likely, on powertrain (EV) and connectivity. But the long-expected low-cost invasion may never materialize.

To sum up: the new-car market has been moving upscale and continues to do so. Used cars have assumed the role of mass-market transport. Americans will probably buy used through their 20s and 30s, and only start to transition to new in their 40s and 50s. When you read that next letter to Car & Driver moaning about “Why doesn’t Detroit make a good cheap car anymore? I’d buy one!” — don’t believe it. America wants premium wheels, when it comes to new cars. Plan accordingly.

Next time around: August grab bag. Three fun factoids, charted. Easy beach reading (assuming you drove your Bronco onto the beach)!

Note: on the impact of the chip shortage on all this. Certainly the shortage has accelerated the upscaling trend: if Americans will buy anything right now (because there are so few cars available), we might as well sell them more profitable, more expensive models and trim levels. Why use scarce chips in a subcompact if I can deploy them into an upscale SUV? And the result has been record profits, as we all know, at least for dealers and OEMs (it is unclear that suppliers have benefited as much). So arguably the single most important question facing OEMs right now is not something trendy about EVs or AVs or mobility or anything else like that, but rather “Can we persuade people to keep paying up, even as supply returns?” Nothing else matters more, and we’ll discuss this in a future post. My gut feel is prices and margins will regress to the mean in a year or two, but that that mean will still be rising, as the upscaling trend rolls on, and the situation may remain quite favorable. Colin Langan at Wells Fargo seems to indicate the same view: we’ll fall back, but to a higher base:

I will focus on 2019 as the last pre-Covid year, for comparability with earlier years, but as we shall see the pandemic and related chip shortage only accelerated the upscaling trend I argue for.

The rest of the world may waft along in silky Benz limos, but our plutocrats are out herding cattle from their King Ranch F-150s, using their 640 watts of onboard Bang & Olufsen stereo to blast ‘em with Jerry Jeff Walker!

This is a relatively new phenomenon. In 2012 less than 5% of Ford vehicles had MSRPs above $50,000, and now 20% do. Yes, there has been inflation, but the real driver of this has been the truck boom (and to some extent the luxury SUV boom). It certainly can’t be chalked up to surging Mercury or Lincoln sales…

When Covid hit, that figure fell to 9.5% in 2020, as OEMs realized customers would buy anything with wheels — so why offer them a lower-margin cheap car? More on this later.

The old joke: “Europeans buy cars, Americans manage fleets.”

Yes, yes, I know about this, but it’s not what I meant: